For many, the idea of retiring at age 50 sounds amazing. However, many question if it is even realistic. Considering that anyone born after 1960 won’t qualify for full Social Security benefits until age 67, that leaves 17 years before they could access that source of income if they stop working at age 50. Plus, most retirement accounts – like 401(k) and IRA accounts – won’t allow you to make withdrawals without penalties until age 59 ½, leaving an 8 ½-year gap. But, even with that, that doesn’t mean retiring at age 50 isn’t possible. In fact, here are four simples things you can do put yourself on the right track.

How to Retire at Age 50

If your goal is to retire at age 50, you’ll need to start planning immediately. If you don’t plan on working once you retire, you have to have enough saved to cover the rest of your life.

With the average U.S. life expectancy now averaging 78.4 years (per the CDC), plan for 28+ years of expenses—potentially 35+ if you’re healthy and active. So you’ll have to plan for having enough money to support yourself (and possibly your household, for 28 years or longer.

The 28 to 35 years is a good rule of thumb. However, if you want to know how many years you specifically have left, the Social Security Administration has a handy calculator here.

As daunting as that may seem, saving for 28 to 36 years of expenses is doable. It just requires some planning, diligence, and dedication. Here’s how to get started.

1. Save as Much as Possible

Retiring early requires a substantial amount of savings. Along with having a robust retirement account, giving you something you can tap once you reach age 59 ½, you’ll need another source of funds to cover that 8 ½-year gap.

Many who aim to retire at age 50 open investment accounts beyond their retirement savings vehicles. Often, these accrue more in interest than traditional savings accounts, allowing your money to grow more quickly. However, they aren’t risk-free, so you need to consider your risk tolerance and choose options that are right for you. For example, investing in index funds, target-date funds, and many mutual funds provide a level of diversification, so they may be a good place to start if you are new to investing.

2. Reduce Your Expenses & Boost Your Income

The less you need to spend each month, the less you’ll need to save. Tackle as much debt as possible before you reach age 50, and the goal becomes more realistic. Similarly, consider cutting back on unnecessary services, like premium cable packages, or other high-dollar expenses, like dining out, to make retiring early more manageable.

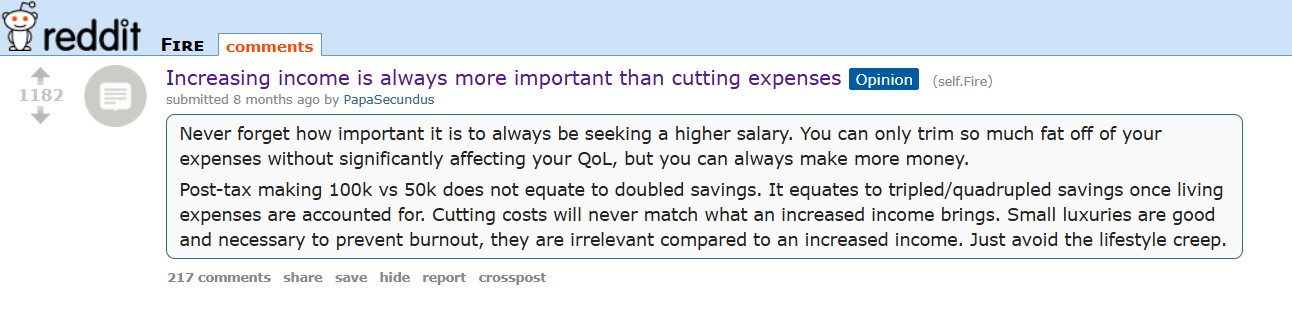

Consider boosting your income as well. Getting a second job, starting a side business or negotiating with your job for a raise are all good ideas for realistically supplementing your income. In fact some commentators note that aspiring retirees can only save so much, whereas improving ones income theoretically has no upper limit. Reddit user PapaSecundus mentions this:

3. Calculate Your Post-Retirement Spending

In order to determine how much you will need to save, you need to understand what you’ll spend in retirement. This includes everything from debt payments to household expenses to medical costs. Plus, you need to account for any changes to your entertainment-oriented expenses. When you retire, you may want to travel, see more movies at the theater, or embrace a hobby, all of which can impact your spending estimates.

You’ll also have to contend with inflation, something that can significantly impact your spending power over time. Inflation has averaged 2.8% percent per year. This means that if you need $50,000 per year right now, you might need $66,000 in ten years. The Bureau of Labot Statistics has a handy inflation calculator here.

Planning for healthcare costs can be especially challenging. You won’t have access to Medicare until you are eligible for Social Security benefits. Even if your employee has post-retirement medical options available, the premiums are usually higher than they would be if you are still working, so you need to explore your options thoroughly to estimate the cost.

Once you calculate your spending, you can use that information to extrapolate how much you need to save. Usually, planning to use a withdrawal rate of 2 to 4 percent is a smart move. If you want to be conservative and use the 2 percent rate and estimate you’ll need $50,000 a year, then you’d have to save $2.5 million before you reach age 50 if that’s when you want to retire.

4. Consider a Partial Retirement

If you can’t save enough to fully retire at age 50, that doesn’t mean you can’t dramatically change your relationship with the working world by then. For example, you may be able to save enough to cover part of your expenses and then opt to work at a job you enjoy on a part-time basis until Social Security kicks in or you can access other retirement savings. Not only will this provide you with some flexibility and additional income, but it also gives you more time to lower your expenses and save.

Then, when you reach age 59 1/2, 67, or anything in between, you can reassess and shift to a full retirement if it is viable. That way, you can change your lifestyle earlier, making your years feel more fulfilling and rewarding.

At what age do you think you will retire? Does 50 sound realistic or even possible for you? Share your thoughts in the comments below.

You Might Also Enjoy….

- Are Seniors Saving Enough to Retire Comfortably?

- Taxes in Retirement Can Make a Big Difference

- Only 37% of Millennials Have Retirement Accounts

- The IRS Can Now Touch More Than Your Bank Account

- Eighteen Percent of US Households Are Millionaires, Are You One?

Read the full article here